The commercial real estate crisis is looming large as high office vacancy rates continue to plague urban centers, raising alarm bells among economists and investors alike. As many businesses shift away from traditional office spaces in the wake of the pandemic, vacancy rates have soared, affecting property values significantly. This crisis not only jeopardizes investments in commercial properties but may also pose serious economic consequences, especially if banks begin to feel the strain of maturing commercial mortgage loans in the years ahead. Compounding this issue are rising interest rates that further deter both investors and tenants, creating a precarious environment for the banking sector. With the stakes high, understanding the economic impact of real estate has never been more crucial as we navigate these turbulent waters.

The ongoing turmoil in the market for commercial properties presents significant challenges that could reshape our economic landscape. As demand for office spaces dwindles in the post-pandemic world, cities are witnessing a concerning rise in vacancy levels, triggering broader reflections on the financial health of various institutions. The ramifications of this downturn are not limited to property values alone, but extend into the banking sector, where risks associated with commercial loans loom large. With interest rates on the rise, the landscape for securing loans is becoming increasingly treacherous, prompting fears of potential delinquencies. As we explore these dynamics, it becomes essential to recognize the multifaceted implications of a faltering commercial real estate sector on the overall economy.

The Impact of High Office Vacancy Rates on the Economy

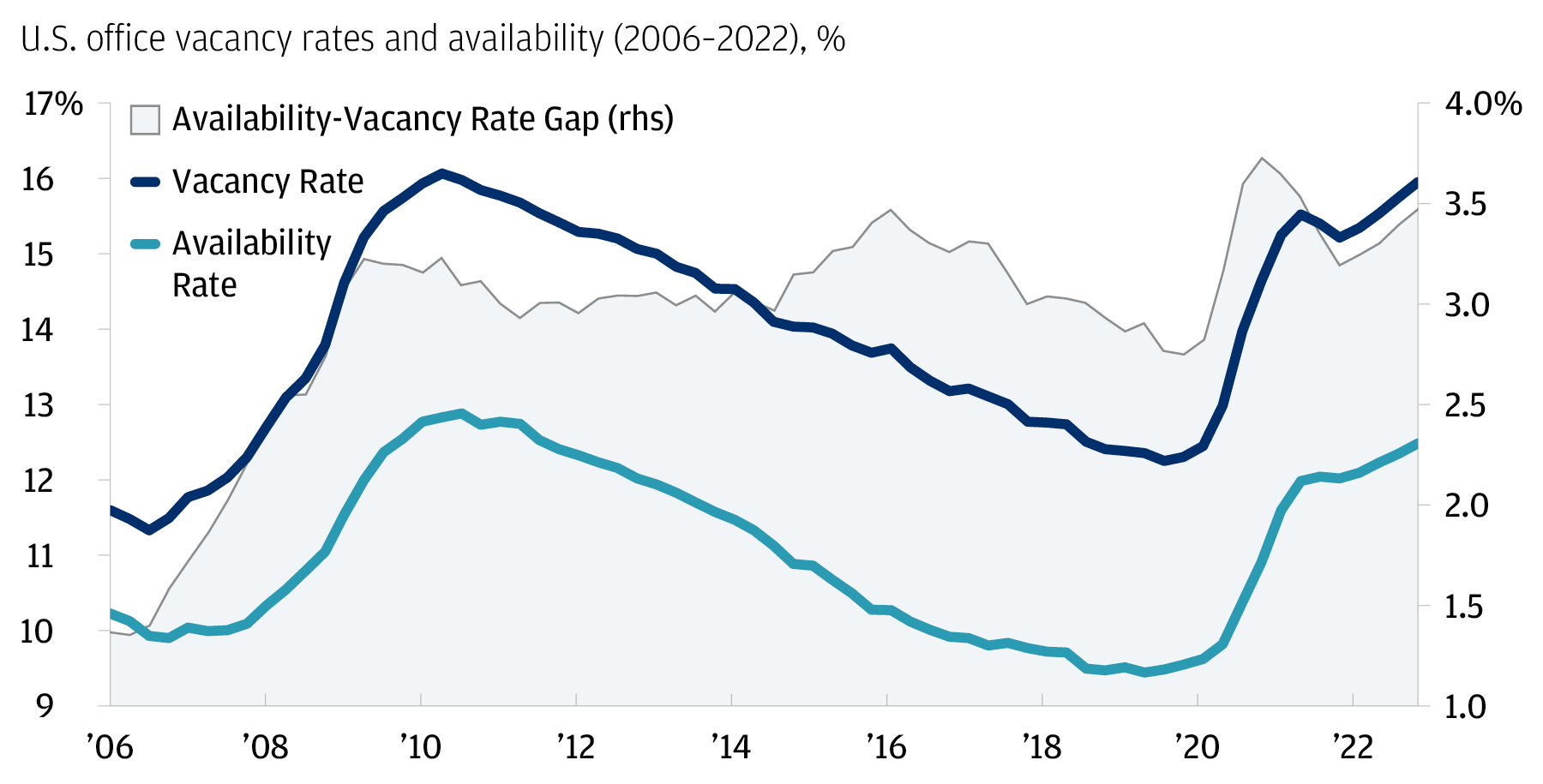

As the demand for downtown office space continues to dwindle, high office vacancy rates have become a significant concern for economic stability. Reports indicate that vacancy rates in major U.S. cities, such as Boston, range from 12% to 23%. This trend has a direct impact on property values, leading to decreased tax revenues for municipalities and a potential slowdown in local economies. When empty office buildings dot the skyline, businesses that rely on foot traffic, such as restaurants and retail stores, also suffer, thereby exacerbating the economic decline in these areas.

The economic repercussions of these high office vacancy rates reverberate through various sectors. For example, local businesses face decreased patronage, which may force them to close or reduce their workforce. This not only affects employees and their families, but it also translates into lower consumer spending, stunting economic growth. Therefore, the ongoing crisis in office occupancy signals a larger problem that extends beyond the real estate market and threatens the overall health of the economy.

Frequently Asked Questions

What is the relationship between high office vacancy rates and the commercial real estate crisis?

High office vacancy rates are a significant indicator of the ongoing commercial real estate crisis. As demand for office space has declined, particularly post-pandemic, vacancy rates have soared across major cities, leading to decreased property values and financial strain on owners and investors. This situation can undermine the wider economy as commercial mortgage loans come due, affecting banks and investors.

How do interest rates impact the commercial real estate crisis?

Interest rates play a crucial role in the commercial real estate crisis. When the Federal Reserve keeps interest rates high, it increases borrowing costs for commercial mortgage loans, making it more challenging for property investors to refinance. High interest rates also contribute to the overall financial instability in the sector, exacerbating the effects of rising office vacancy rates and impacting the banking sector.

What are the banking sector risks associated with the commercial real estate crisis?

The commercial real estate crisis poses significant risks to the banking sector, particularly for regional banks heavily invested in commercial mortgage loans. As properties sell for much less than their purchased value due to high vacancy rates, banks may face increased delinquencies on these loans, leading to potential financial distress and bank failures.

What economic impacts can be expected from the commercial real estate crisis?

The commercial real estate crisis could lead to a ripple effect in the economy. Higher office vacancy rates and significant losses in the real estate market may reduce lending capacity from regional banks, subsequently affecting consumer spending and overall economic growth. While some areas may suffer, the current strong job market mitigates widespread economic downturn.

Are we likely to witness a significant financial crisis due to commercial real estate loans?

While the commercial real estate crisis raises concerns about bank stability, a full-blown financial crisis is not necessarily imminent. The situation is severe but not yet comparable to the 2008 financial meltdown. The differentiated levels of regulation for large versus regional banks may prevent widespread systemic failures.

Will declining commercial real estate values lead to a recession?

Declining values in commercial real estate may contribute to economic challenges, but they are not likely to trigger a recession on their own. If significant downturns in regional banks occur, coupled with additional economic stressors, the chances of a recession could increase. However, the current economic landscape has been resilient, with strong job markets aiding in offsetting these effects.

How can the commercial real estate sector recover from its current crisis?

Recovery from the commercial real estate crisis may depend on several factors, including a significant decline in long-term interest rates, which would ease refinancing pressures for investors. Additionally, structural changes in demand, such as repurposing office spaces for residential use, could help stabilize the sector if zoning and engineering challenges can be overcome.

What is the outlook for investors in commercial real estate amidst this crisis?

Investors in commercial real estate face a challenging outlook as high vacancy rates contribute to depreciated property values. However, some investors remain optimistic that long-term interest rates will decrease, which could provide relief through refinancing opportunities. The landscape remains complex, and investors must adapt to evolving market conditions to navigate potential challenges.

How do commercial mortgage loans contribute to the current crisis?

Commercial mortgage loans are a critical factor in the current crisis, with a significant portion coming due in the near future. High office vacancy rates have led to diminished property values, increasing the risk of default on these loans. As lenders confront potential losses, the impact could reverberate through the banking system, particularly affecting smaller banks with higher exposure.

How does the commercial real estate crisis potentially affect pension funds and insurance companies?

Pension funds and insurance companies that hold substantial investments in commercial real estate could face significant losses due to the ongoing crisis. With deteriorating property values and high vacancy rates, the financial health of these institutions is at risk, which, in turn, could affect the financial security of retirees and policyholders.

| Key Points | Details |

|---|---|

| High Vacancy Rates | Office space vacancy rates in major cities range from 12% to 23%, affecting property values. |

| Commercial Real Estate Debt | 20% of $4.7 trillion in commercial mortgage debt is due this year, raising alarms about potential delinquencies. |

| Effects on Banks | While large banks have been regulated to avoid crises, smaller banks are more vulnerable to potential failures. |

| Long-term Outlook | Experts suggest that without a significant recession, the real estate crisis won’t lead to a full-blown financial meltdown. |

| Market Reactions | High interest rates may lead to increased bankruptcies in real estate, affecting consumers through pension fund losses. |

Summary

The commercial real estate crisis showcases a precarious situation, where high office-vacancy rates combined with a swelling debt maturity schedule could lead to substantial challenges for banks and the economy at large. Although some experts predict doom, they also point out that the impact may not be as catastrophic as that of the 2008 financial crisis, particularly for larger banks that are more resilient. Ultimately, the commercial real estate sector’s performance will hinge on interest rate fluctuations and market adjustments, underlining the importance of strategic oversight in navigating this evolving economic landscape.